隨著世界的不斷全球化,進軍商業世界的有志人士也在日益增多。其直接結果是,人們已經廣泛認識到,對於企業如何識別和呈現其財務信息達成普遍共識是至關重要的。財務報告準則有助於解決此問題,因為它們提供了最低程度的透明性和對企業如何識別和呈現其財務信息的理解。現在,預計所有國家都將採用僅以此為依據的財務報告準則,香港也不例外。在本文中,我們將探討什麼是香港財務報告準則,其影響範圍以及中小企業所有者應考慮的事項。

本文內容包含:

2. 香港財務報告準則的範圍是什麼?

根據香港會計師公會,香港財務報告準則旨在適用於所有以利潤為導向的實體的通用財務報表和其他財務報告。

以利潤為導向的實體包括從事商業、金融和類似活動的實體。《香港財務報告準則》不適用於私營部門、公共部門或政府的非營利活動。

4. 香港財務報告準則的主要原則

會計的權責發生制

香港的會計制度獨特之處在於,香港公司將使用應計制會計基礎,但是現金流量表是一個例外。這意味著,導致重大會計變更的交易和事件的影響應在發生時予以確認。

在此基礎上編制的財務報表不僅向用戶顯示了涉及現金支付和接收的過往交易,而且還告知用戶將來支付現金的義務以及代表將來將要接收的現金的資源。

香港財務報告準則第1條:財務報表的呈列

香港財務報告準則第1條在呈列財務報表時指明整體要求,並就其內容及其內容的最低披露規定提供指引。

總結香港財務報告準則第1條:

- 編制實體的財務報表時,管理層應評估實體持續經營的能力。

- 當實體不按照持續經營的基礎編制財務報表時,應披露該事實並說明為何以這種方式編制財務報表。

- 除非香港財務報告準則要求或允許,否則實體不得抵銷資產和負債或收入和支出

- 實體每年至少應提交一套完整的財務報表(包括比較信息)

香港財務報告準則第2條:存貨

香港財務報告準則第2條從會計角度闡述應如何處理存貨。在香港,主要標準是將存貨確認為一項資產並按成本確認,並且這些資產應結轉至確認相關收入。

- 存貨按照成本與可變現淨值兩者中的較低者計量。

- 存貨成本應包括所有購置成本、轉換成本以及將存貨轉移至當前位置和狀態所發生的其他成本。

- 存貨成本應採用先進先出或加權平均成本公式進行分配。

香港財務報告準則第18條:收入

香港財務報告準則第18條闡明了在某些類型的交易和事件中產生收入時應如何處理。

- 收入應按已收或應收對價的公允價值計量

- 滿足以下所有條件時,應確認商品銷售收入:

- 實體向買方轉移了貨物所有權的重大風險和報酬

- 該實體既不保留與所有權通常相關的程度的持續管理參與,也不保留對所售商品的有效控制

- 可以可靠地計量收入金額

- 與交易有關的經濟利益很可能流入實體

- 可以可靠地計量與交易有關的已發生或將要發生的成本

有關整套《香港財務報告準則》,請參閱香港會計師公會的《香港財務報告準則》手冊。

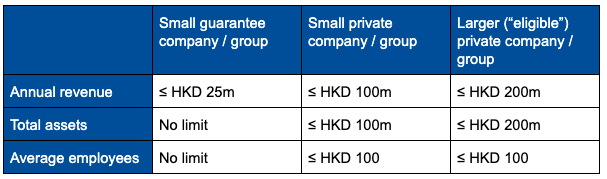

5. 中小企香港財務報告準則

香港財務報告準則公會還發布了針對中小型企業的報告框架,被稱為《中小企業財務報告框架》(“ SME-FRF”)和《中小企業財務報告標準》(“ SME-FRS”)。

符合香港豁免申報資格的中小型企業

在香港註冊成立的公司,如果符合以下報告豁免標準,則符合SME-FRF和SME-FRS規定的報告資格:

- 它們通過規模測試; 和

- 如果是大型私人公司,則至少要獲得75%的股東批准,且無人反對

受擔保限制的香港公司和私人公司可能有資格獲得可選的報告豁免。在以下情況下,中小型企業將無資格獲得報告豁免:

- 中小企業是根據《銀行業條例》授權的機構;根據《證券及期貨條例》第V部,該實體獲准從事受規管的業務活動

- 該公司從事任何保險業務,但不包括代理商開展的業務

- 公司接受作為商業或貿易一部分的利息或溢價償還的貸款。 這不包括涉及債券和證券的條款

在SME-FRF和SME-FRS下,香港公司無需提供真實、公正地了解其金融交易的要求。借助簡化的財務報表,中小企業可以:

- 可能根據SME-FRF和SME-FRS <而不是HKFRS來準備財務報表

- 這意味著中小型企業的財務報表以簡化的歷史成本為基礎編制,不包括任何公允價值或遞延稅項的資產或負債。

- 與完整的財務報表相比,披露說明中包含的與報告實體事務相關的信息也更少

結語

由於使用財務報告準則可以大致了解企業的經營狀況,因此了解並遵循當地的財務報告準則至關重要。如果不遵循這些標準,企業就有可能無法正確地將其呈現給利益相關者。有關香港財務報告準則將如何影響您的業務的疑問,請聯繫永捷集團尋求幫助!